Over the past few decades, Americans have taken on increasing amounts of debt to get by. About 80 percent of American households now hold some form of debt, according to the�Pew Charitable Trusts' survey of American family finances. And less than half, or 46 percent, reported making more than they spend.

But when you are short on cash, not all types of borrowing are created equal. Here are some of the best and worst loans out there.

More: 9 things to know about your credit score and how it's calculated

More: Personal savings: 40 pretty easy ways to spend less money

More: 401(k) limits: 7 answers to your top retirement plan questions

A pile of four different credit cards. (Photo: Getty Images)

Credit cardsCredit cards are one of the most common �� and also one of the most expensive �� ways to borrow money. Because card issuers charge much higher interest rates than other types of lenders, carrying a credit card balance can quickly escalate out of control.

Currently, credit card rates are at a record high, at an average of about 17 percent, according to Bankrate, and the average American has a credit card balance of $6,375, up nearly 3 percent from last year, according to�Experian's annual study on the state of credit and debt in America.

.oembed-asset-photo-image { width: 100%; }

Good credit card management boils down to making payments on time and relying on revolving credit only in limited situations, according to Greg McBride, Bankrate.com's chief financial analyst.

If you are planning a big purchase, like a large appliance for example, a zero-introductory credit card offer could be a worthwhile way to secure a short-term loan with no interest, as long as the purchase is paid off by the time the introductory period ends, he said.

Otherwise, only buy things with plastic that you can afford to pay off at the end of the month.

More: How to get a credit card when you've never had one

Home equityBefore the Great Recession and the historic housing crash, homeowners used their homes to access as much cash as the bank would allow. But borrowers who were burned by falling housing prices, not to mention today's tighter lending standards, are considerably more wary now when it comes to home equity loans and lines of credit �� despite the more favorable terms.

Still, the amount of equity today's homeowners are able to tap is at�the highest level on record.

One of the most common ways to tap that equity is through a cash-out refinance (which is when you refinance your current mortgage and take out a bigger mortgage) or a home equity loan.

A home equity loan can be withdrawn as a lump sum with a fixed rate and a repayment period generally of five to 15 years or as a home equity line of credit with a variable rate.

The average interest rate on a home equity loan is 5 percent to 6 percent, but under the new tax law the money must be used to improve your home, otherwise the interest is not tax deductible.

More: Home equity hits record high, and here's how homeowners are spending it

CLOSESummer season means outdoor fun but it��s important to avoid getting caught up in all the excitement when it comes to summer spending. Buzz60's Maria Mercedes Galuppo has more. Buzz60

Personal loansPersonal loans, or unsecured loans, do not require borrowing against something of value, like a house, which makes them particularly attractive for those without that kind of equity. However, that generally means the loans are available at a higher interest rate than a home equity loan.

Personal loans are also locked in over shorter terms, like one to five years, and payments are generally automatically deducted from a checking account, which decreases the odds of missing a payment or defaulting.

Personal loans are well suited for smaller loan amounts than a typical home equity loan, but more than one would want to run up on credit cards �� generally, anything up to $35,000.

A number of online lenders, like Lending Club and Prosper, have popped up in recent years to offer these types of loans as another way to borrow money, particularly for millennials who may want to consolidate their debt but don't have the home equity for a secured loan to do it.

The average interest rate on an unsecured loan is currently about 11 percent, according to Bankrate, although those with very good credit can get a rate as low as 5.5 percent. That's notably less than the APR on a credit card.

More: Credit card debt vs. 401(k) investing: Which should you focus your financial resources on?

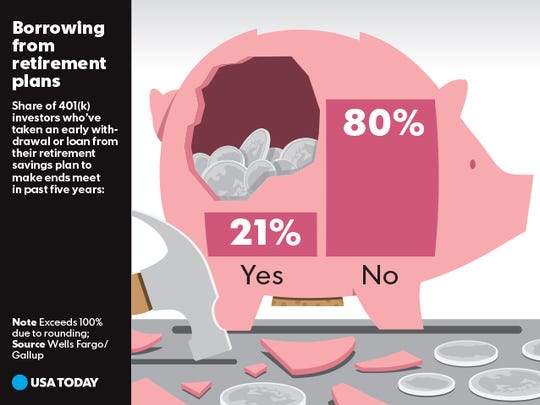

Borrowing from retirement plans (Photo: USA TODAY)

Tapping a 401(k)Although many financial advisors say 401(k) loans should be off-limits entirely, federal law allows workers to borrow up to 50 percent of their account balance, with a maximum of $50,000.

Borrowers then have up to five years to pay back their loan, which comes with an interest rate that typically is lower than other with other borrowed money, such as credit cards.

“A 401(k) loan sounds innocent enough, but it is a permanent setback to your retirement planning.”

Greg McBride, Bankrate's chief financial analystThere is a significant downside to borrowing from your own retirement account. ��A 401(k) loan sounds innocent enough, but it is a permanent setback to your retirement planning,�� McBride said.

��You spend resources replacing money you borrowed instead of making new contributions, and you miss out on potential capital gains, dividends and interest income during the time the loan in outstanding.��

On top of that, if you leave your employer, by choice or otherwise, the loan balance will be due within 90 days.

漏�CNBC�is a USA TODAY content partner offering financial news and commentary. Its content is produced independently of USA TODAY.

More from CNBC:

Why squirreling away every spare dime into your 401(k) is a bad idea

This move is almost as bad for your retirement savings as the Great Recession was

July Fourth car shopping? Avoid these five big mistakes

No comments:

Post a Comment